Millenium Home Mortgage LLC

Millenium Home Mortgage LLC

The hidden costs of homeownership in high-risk areas

___

Published Date 7/12/2024

When Dorothy got knocked senseless in a movie tornado, experienced the amazing land of Oz, and woke up to smiling faces back in Kansas, it’s doubtful she understood the aftermath and expense of what the weather left behind for her family to deal with.

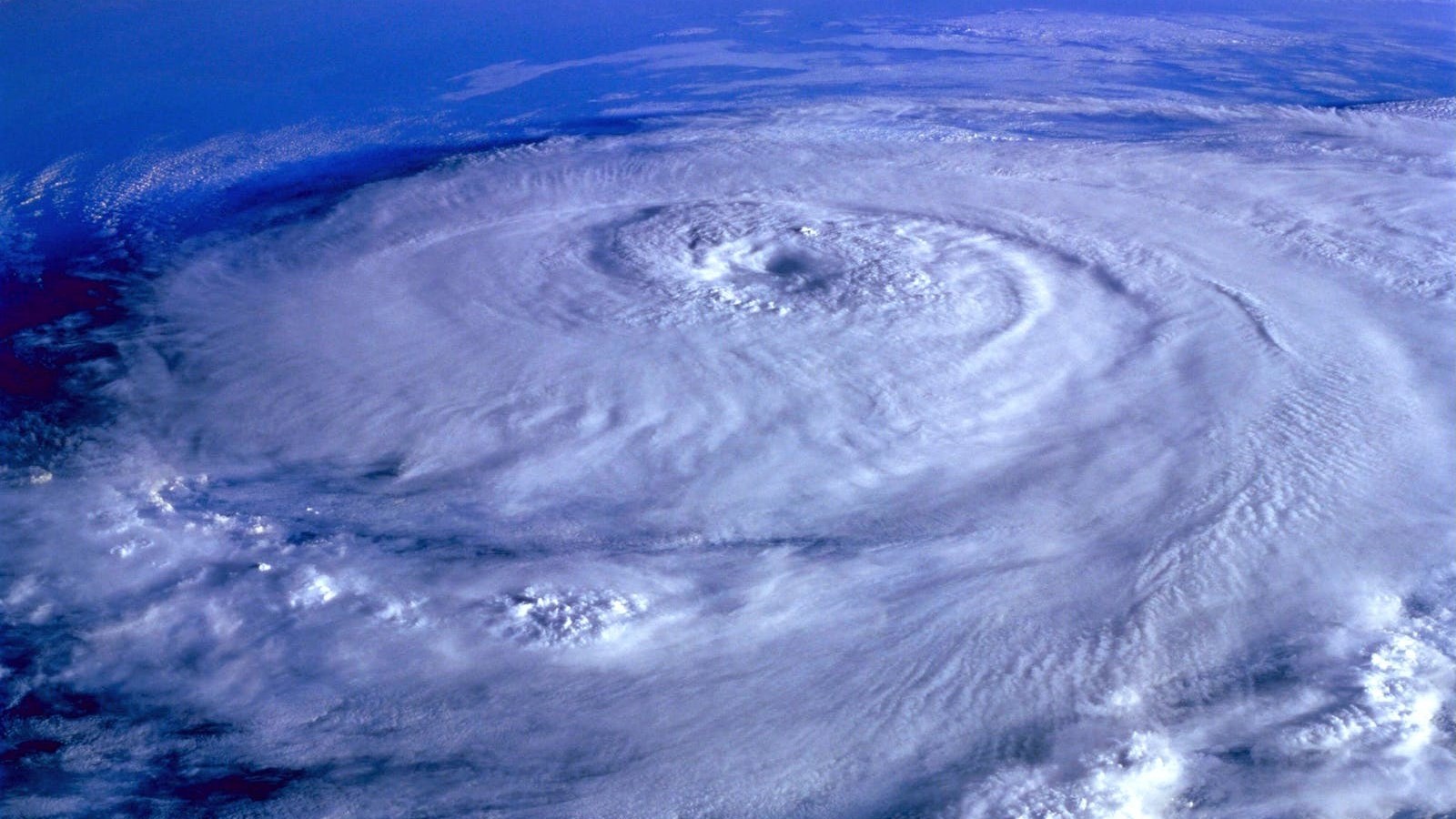

According to a recent Realtor.com report, approximately 18.1% of homes in the country—mainly in Louisiana, South Carolina, Florida, and Texas—face potential damage from hurricanes and tornadoes. Beyond that, 19 states plus Washington, DC, require additional hurricane deductibles, raising the cost of repairing the damage when it happens.

Realtor’s Liz Brumer-Smith, a native Floridian and resident, says that while she lives with the fear of getting hit with a hurricane, it wasn’t until she bought her first house in St. Petersburg in 2023 that she faced another grim realization: the hidden costs of owning a home in a storm-prone area.

Whatever has you relocating and buying a home in one of these states, it’s important you’re ready to incur some of the curveball costs. Brumer-Smith bases this on her own experience as well as that of other homeowners who’ve lived through hurricanes.

As a kid living through hurricane season, events like evacuations may have seemed like an adventure. But as a homeowner, it would become a different story, according to Louisiana resident Gary Dardar, who advises that protecting your home’s windows is one of the most important things to do before a hurricane. Plywood is the most cost effective, while hurricane shutters (which cost several hundred to several thousand to be fit and installed on all openings) serve as optimal protection. While Dardar installed impact windows, he still boards up everything no matter the size or strength of the storm.

Is your home close to the water in a hurricane zone? If so, there’s a chance your county will require impact windows. Brumer-Smith says in Pinellas County, where she lives, the required impact-rated windows she is about to install to replace some of her original 1947 windows are slated to cost anywhere from $14,000 to $27,000.

Power outages can last several days to several weeks. Dardar evacuates for most storms since they have an RV they can easily escape in. “But we also purchased two generators for after we return, which cost close to $1,000,” he says. “Then we have fuel to run those generators every day.”

Upgrades to an electrical panel to keep power going after a storm might seem unnecessary, but if comfort is key, it can power things like your air conditioner to help you get through any hot and humid nights, or keep your food cold for longer periods.

If you are one of those who evacuates only under the most dire of circumstances, a well-stocked hurricane kit is a must. “This cost is minimal compared with some of the other hidden expenses, but it’s worth mentioning,” says Brumer-Smith. “This includes nonperishable food, drinking water, first-aid kits, life vests, flashlights and batteries, candles, and matches.” Those who lived through hurricanes report that they were glad to have a few items such as a cast-iron skillet, a grill with materials to light it, a clothesline and clothespins, life jackets, and coolers.

And then there is home insurance — a topic of great discussion among homeowners, Realtors, and those thinking of moving to a hurricane zone. Not surprisingly, home insurance costs in high-risk areas are skyrocketing. “New building codes require homes to be built to higher wind-rating standards and on stilts, Says Brumer-Smith. “If your home doesn’t meet these requirements, it can be notably more expensive to insure—if you can get insured at all.”

After Hurricanes Laura and Delta, the Dardars went through their insurance to replace their damaged roof. Insurance covered the entire cost, but then their premium increased by 29%. And since they’re in a flood zone, the Dardars have to pay for flood insurance in addition to homeowners insurance — an amount almost as much as their mortgage.

When Brumer-Smith and her family closed escrow on her home in 2023, she shopped around for insurance and was shocked to see quotes in the $5,000 to $7,000 range. “This was way higher than I ever imagined, particularly because we’re not in a flood zone and our single-family home is relatively small at 1,000 square feet.” Although she ended up getting a rate just under $3,000 with a state-funded insurance program designed to temporarily help homeowners who cannot afford a private insurance company, it’s not the best coverage. And that company now says it will require all homeowners to carry flood insurance by 2027, which will raise her premiums if a storm doesn’t come along and force the company to drop her coverage first.

Repair costs are all over the map. Removing old trees or branches that have fallen on a house can cost up to $25,000 — in addition to living expenses no one will pay for if you can’t inhabit the place. And while repairs like this might be covered by insurance, the homeowner might not get fully reimbursed.

Labor costs skyrocket when repairs are needed due to a surge in demand. “After a storm, it’s extremely difficult to find qualified workers to help repair your home,” says Dardar. “They tell you they are licensed contractors, but they may be scamming you. They can also price-gouge.” He tells the story of how Hurricane Ida hit Southwest Louisiana in 2022. “My aunt’s house is still without a roof two years later because the insurance company went bankrupt. She never got anything.”

In the end, it’s about preparedness for just about everything, including a healthy savings account to cover anything insurance will not step up to the plate to help with.

Realtor, TBWS

All information furnished has been forwarded to you and is provided by thetbwsgroup only for informational purposes. Forecasting shall be considered as events which may be expected but not guaranteed. Neither the forwarding party and/or company nor thetbwsgroup assume any responsibility to any person who relies on information or forecasting contained in this report and disclaims all liability in respect to decisions or actions, or lack thereof based on any or all of the contents of this report.

Millenium Home Mortgage

Manager

NMLS: 51519

Millenium Home Mortgage LLC

1719 Route 10 East, Suite 206, Parsippany NJ

Company NMLS: 51519

Office: 973-402-9112

Email: connie@mhmlender.com